Emotional Intelligence and Gen Z’s Insurance Choices

Anushka Sarkar1, Dhiksha A2*, Neil Mathews Koshy3, Shaeril Michael Almedia4

DOI:10.5281/zenodo.15099294

1 Anushka Sarkar, Final Year B.Com Honours Student, Department of Commerce, Christ University, Bengaluru, Karnataka, India.

2* Dhiksha A, Final Year B.com Honours Student, Department of Commerce, Christ University, Bengaluru, Karnataka, India.

3 Neil Mathews Koshy, Final Year B.Com Honours Student, Department of Commerce, Christ University, Bengaluru, Karnataka, India.

4 Shaeril Michael Almedia, Assistant Professor, Department of Commerce, Christ University, Bengaluru, Karnataka, India.

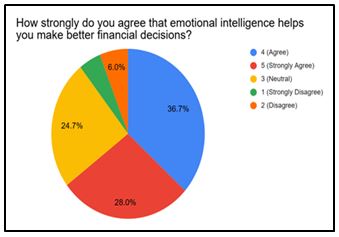

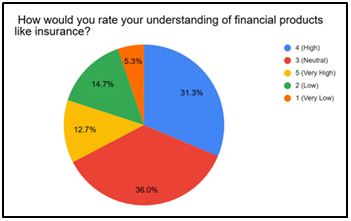

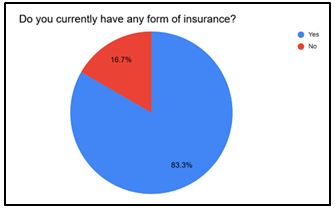

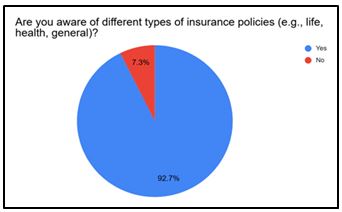

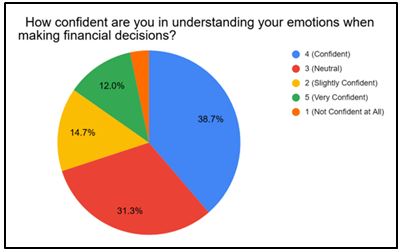

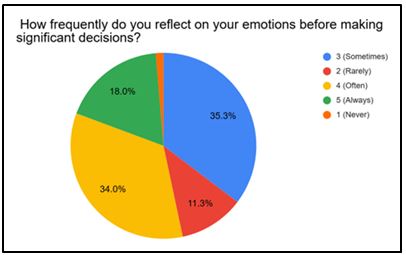

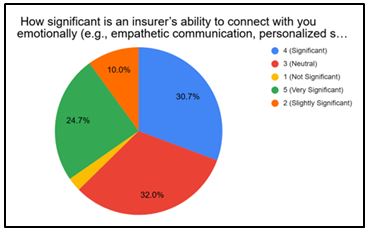

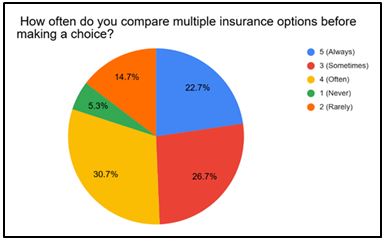

A lack of industry engagement with this tech-savvy but emotionally complex group is evident in the case that only 28% of Gen Z have insurance. This study examines the ways in which trust-building, emotional regulation, and tailored strategies can increase insurance uptake. Using both theoretical and empirical analysis, it looks at how Gen Z's insurance mindset and emotional intelligence (EI) match up. Trust and awareness are increased by EI-focused tactics like sympathetic communication and customised financial responses. Insurers can boost adoption and promote sustained engagement by attending to Gen Z's emotional needs and digital preferences.

Keywords: generation z, emotional intelligence, insurance adoption, consumer behavior, trust-building, emotional regulation, customized engagement, digital literacy, ei-based marketing, decision-making, financial services, long-term engagement

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Final Year B.com Honours Student, Department of Commerce, Christ University, Bengaluru, Karnataka, India. Email:  |

Anushka Sarkar, Dhiksha A, Neil Mathews Koshy, Shaeril Michael Almedia, Emotional Intelligence and Gen Z’s Insurance Choices. soc. sci. j. adv. res.. 2025;5(2):1-11. Available From https://ssjar.singhpublication.com/index.php/ojs/article/view/227 |

|

©

©